Penny Drop Verification

Streamline compliant user identity and bank account verification processes today.

Penny Drop Verification is Sumsub's document-free data verification solution designed to deliver a real-time API connection to customer banking information on a pan-European level through a nominal monetary transfer.

The solution is based on the Payment Initiation Service (PIS) under the EU/EEA open banking technical infrastructure, which allows authorized Third Party Providers (TPPs) to securely access consolidated information from a customer's payment account in 28 countries and over 550 financial institutions. As a result, Penny Drop Verification covers over 90% of the adult population in each supported jurisdiction, as it successfully represents all residents that have an active account in any one of the available banks.

Penny Drop Verification solution works by simply having the applicant authenticate themselves on their selected banking platform via a standard login process and confirm a nominal payment to Sumsub's digital account, which is instantly processed and refunded shortly after. The result delivers comprehensive customer account ownership and transaction details, as well as a confirmation of their real-time presence in compliance with a range of use cases under the AML/CTF and the Revised Payment Services Directive (PSD2), including Identity, Payment Method, and Qualified Electronic Signature (QES) Verification.

Overall, Penny Drop Account offers one of the most well-recognized solutions to customer banking data verification that helps businesses achieve international AML/CTF and PSD2 compliance, prevent identity fraud, and optimize due diligence procedures, all through a seamless, document-free user experience.

Note

- The open banking infrastructure under the Directive (EU) 2015/2366, officially referred to as the Revised Payment Services Directive (PSD2), is a technological and legal framework which mandates Account Servicing Payment Service Providers (ASPSPs) in the European Economic Area (EEA), including banks, credit institutions, and electronic money institutions, to allow authorized Third Party Providers (TPPs) access to financial customer data via application programming interfaces (APIs) on the basis of explicit customer consent. TPPs consist of Payment Initiation Service Providers (PISPs), Account Information Service Providers (AISPs), and Card-Based Payment Instrument Issuers (CBPIIs).

- Sumsub offers its solution by leveraging the Payment Initiation Service (PIS) through Volt, a licensed and PSD2-compliant PISP. As a result, Sumsub itself is not subject to the PSD2 regulatory obligations.

- All payment transactions are conducted using Sumsub's Virtual Account on the Volt platform by default. Clients that would like to set up and use their own Virtual Account with Volt should inform their Customer Success Manager about it. This option requires passing an additional due diligence process and executing a supplementary Service Agreement with Volt, Sumsub acting as the supporting intermediary. The process takes around 2-3 weeks to complete. Once the Virtual Account is created, Sumsub will use the client's API key to enable the solution.

- The solution currently facilitates connectivity to banking institutions that process Euro (EUR) currency transactions.

- The current nominal transaction amount is set to 0.10 EUR; however, this may be increased in the future, provided Sumsub encounters cases with banks that do not process such small transactions.

- The Penny Drop Verification solution is only supported via the WebSDK, which requires redirecting to an external browser (for example, Chrome, Safari) to function correctly. It is not compatible with application-embedded browser environments, including WebView components (Android WebView and iOS WKWebView) as well as browser presentation components (Android Chrome Custom Tabs and iOS SFSafariViewController).

Use cases

Penny Drop Verification satisfies three primary use cases for Sumsub clients.

Case 1: User onboarding

Penny Drop Verification lets you stay compliant with national AML/CTF regulations in the European Union, including France, Germany, Spain, Italy, and other countries:

- Banking institutions

- E-money institutions

- Trading platforms

- iGaming operators

- Investment platforms

- Credit unions

- Brokerage firms

- Insurance companies

Case 2: Qualified electronic document signing

Penny Drop Verification is part of the signing process. Thus, it facilitates the execution of high-value/high-risk operations that require the same legal power as a handwritten signature, especially in Germany:

- Financial Services — credit applications, platform usage agreements, loan agreements.

- Employment — employment contracts, vendor contracts.

- Government — permits, tax returns.

- Healthcare — patient consent forms, prescriptions.

- Real Estate — property leases, sales agreements.

Case 3: Payment method verification

Penny Drop Verification adds to customer bank account data checks, including ownership, account number, and banking institution details:

- Banking institutions

- E-money institutions

- Trading platforms

- iGaming operators

- Investment platforms

- Credit unions

- Brokerage firms

- Insurance companies

Solution benefits

Penny Drop Verification is valuable for all businesses enrolling new customers.

Key benefits of the Sumsub Penny Drop Verification solution include the following:

- Coverage. Reach verified records of over 90% of the national adult population in each of the 28 supported countries with the use of a single solution.

- Compliance. Meet international CDD and EDD requirements under AML/CTF, PSD2, and upcoming European regulatory mandates.

- Scalability. Onboard customers on a pan-European level, without having to comply with country-specific standards, such as ANSSI in France, SEPBLAC in Spain, and ADR in Romania.

- Conversion. Improve the speed and user experience of user verification in comparison to traditional methods, leading to a direct increase in both customer conversion and approval rates.

- Fraud Prevention. Verify customer data legitimacy, minimizing the risk of identity fraud, such as account takeover or illicit use of payment credentials via SCA and data cross-matching features.

- Seamless Integration. Seamlessly integrate Sumsub's solution into your system via our lightweight Mobile and Web SDK frameworks.

How Penny Drop Verification works

Sumsub's Penny Drop Verification is an advanced customer banking data verification solution that enables a real-time API connection to customer banking information on a pan-European level via a nominal monetary transfer.

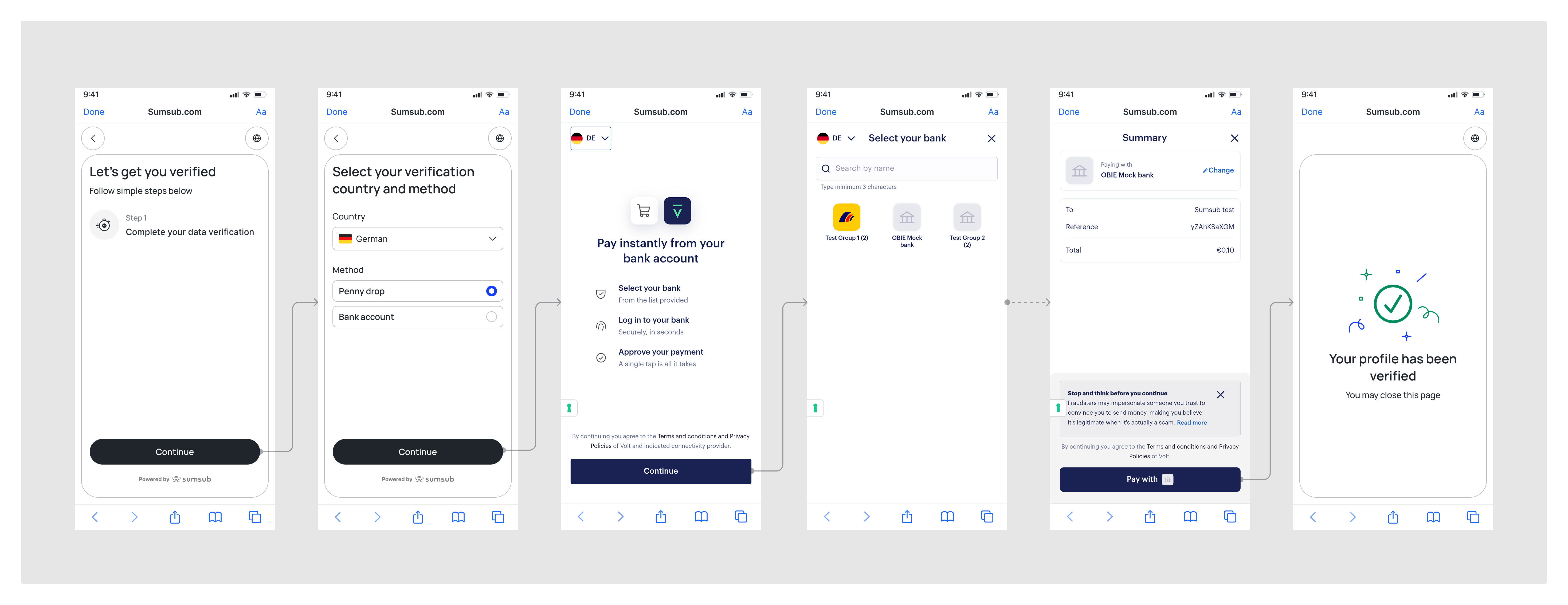

Step-by-step product journey

- Country and bank account selection. An applicant selects their country and preferred banking platform for verification.

- Bank account login. The applicant logs into their bank account using Strong Customer Authentication (SCA).

- Payment confirmation. The applicant authorizes a nominal payment, typically of 0.10 EUR, to be processed from their account.

- Real-time presence. The relevant applicant identity and account data are retrieved to confirm the applicant's real-time presence.

- Account ownership validation. Sumsub cross-checks the information to ensure a complete identity match and validates the account ownership.

- Payment refund. The system automatically refunds the payment amount to the applicant.

Supported jurisdictions

The Penny Drop Verification solution is supported by the banks of the following jurisdictions:

Explore our Coverage Sheet for a full breakdown of ASPSPs enabled by our Penny Drop Verification solution within each jurisdiction for payment transaction and refund execution.

Compliance overview

The Sumsub Penny Drop Verification solution aligns with critical European regulatory frameworks, ensuring businesses meet compliance requirements while enhancing the security of financial transactions:

- Identity Verification. Fully automated user onboarding in compliance with the national AML/CTF regulatory requirements for customer due diligence in Europe(see the breakdown by country below).

- QES Verification in Germany. Under the requirements of the German Money Laundering Act (GwG § 12 (1) 3.), when a person's identity is verified by means of a Qualified Electronic Signature, the obliged entity is also required to ensure that a transaction is executed directly from a payment account, which is held in the name of the verified individual.

- Payment Method Verification. Under the 4th Anti-Money Laundering Directive (Directive (EU) 2015/849), all regulated institutions whose operations involve payment transaction processing are advised to perform payment method ownership verification in order to combat both money laundering and the financing of terrorist activities. The Penny Drop Verification solution helps businesses ensure the legitimacy and ownership of the payer’s account, providing accurate identification and traceability of any executed transaction. This verification process plays a pivotal role in safeguarding the financial ecosystem against fraud and illicit activities.

- Instant payment processing. All payment service providers (PSPs) in the Single Euro Payments Area (SEPA) are required to offer instant payment transactions as a standard service under the Instant Payments Regulation (Regulation (EU) 2024/886), ensuring they are as accessible as traditional SEPA Credit Transfers. The regulation will become applicable to all EU member countries in the eurozone in October 2025, as well as those outside of the eurozone in July 2027.

For more information on the solution compliance assessment, refer to this article.

Setup and configuration

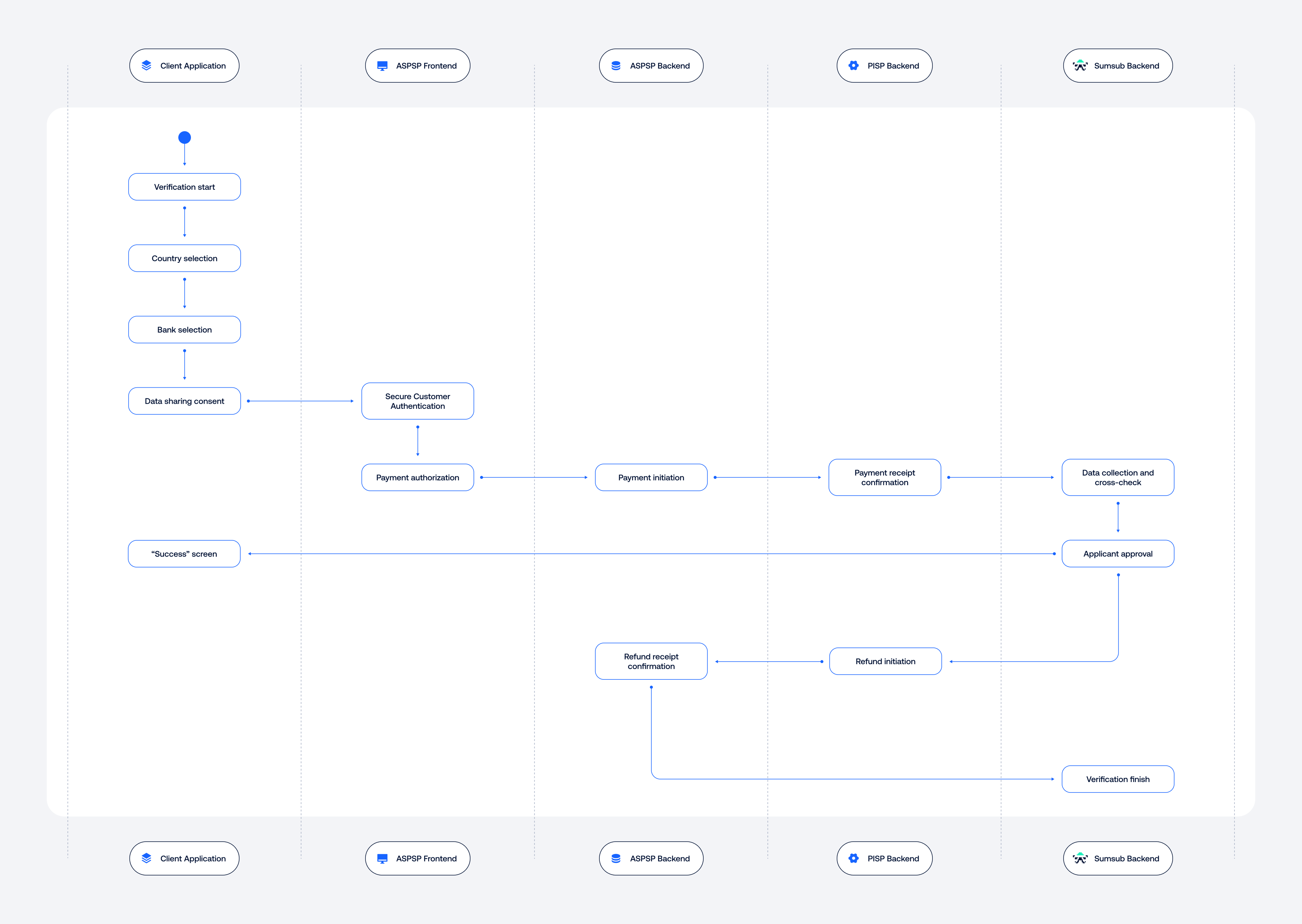

The provided Penny Drop Verification solution scheme demonstrates the following:

- Interaction between Sumsub, our client, applicant, and the bank widget.

- Required and optional steps of the end-user journey.

- Overall solution functionality.

Penny Drop Verification FAQ

Find the most frequently asked questions about Penny Drop Verification.

What is the difference between SEPA Credit Transfer and SEPA Instant payment transfer methods?

The Single Euro Payments Area (SEPA) is a pan-European payment system that enables international bank transfers in the Euro currency across 36 participating countries, including all 27 member states of the EU and Andorra, Iceland, Lichtenstein, Monaco, Montenegro, Norway, San Marino, Switzerland, United Kingdom and the Vatican City. SEPA Credit Transfers typically take 1–2 business days to settle. SEPA Instant, on the other hand, facilitates real-time payments, settling transactions in a matter of seconds, even on weekends and holidays. Currently, each financial institution decides internally on the payment system they adopt, therefore, to avoid delays in customer verification and session drop-offs, Sumsub's Penny Drop Verification solution covers only those banks that process at least 80% of all payment transactions within 30 minutes.

To whose bank account will the payment transaction ultimately be sent?

There are two options:

- If the business opts to use Sumsub's virtual settlement account, the payment will be received by Sumsub and automatically refunded to the end-user.

- If the business chooses to use their own settlement account, the payment will be sent directly to the client’s account. This option requires passing an additional due diligence process and executing a supplementary Service Agreement with Sumsub's partnering Payment Initiation Service Provider (PISP) Volt, Sumsub acting as the supporting intermediary. The process takes around 2-3 weeks to complete.

Which currencies does Penny Drop Verification support for payment transactions?

Currently, Penny Drop Verification only supports transactions made in the Euro (€) currency.

What is the possible range of payment amounts that the end-user may be charged?

The Penny Drop Verification payment amount depends directly on the minimum that is accepted by the internal policies of the customer's ASPSP. This amount typically ranges between 0.10 to 1 EUR.

Are Sumsub clients required to perform any additional actions to enable the Penny Drop Refund feature?

No, this feature will be enabled for all clients using the Penny Drop Verification solution and relying on Sumsub's Virtual Account with Volt.

Will the end-user be charged an additional transfer fee for the payment transaction?

Both SEPA Credit Transfers and SEPA Instant international transfers generally cost the same as local domestic bank transfers, and are often free of charge. However, some financial institutions may charge additional fees, depending on their internal policy. Since Penny Drop Verification only supports Euro-to-Euro transactions, there will be no currency conversion fees involved.

What is the maximum time for payment transaction processing?

The exact processing time depends on the payment system used by the financial institution. Within the SEPA Instant infrastructure, settlements occur within seconds. However, for standard SEPA Credit Transfers or other non-instant methods, processing can take up to 72 hours.

To avoid delays in customer verification and session drop-offs, Sumsub's Penny Drop Verification solution covers only those banks that process at least 80% of all payment transactions within 30 minutes. Nonetheless, our system allows for a maximum of 24 hours for the transaction to be either successfully approved by the payer's ASPSP and received by Sumsub, or rejected due to one of the applicable reasons.

What is the maximum time for refund transaction processing?

While Sumsub's solution processes refunds instantly, the settlement time on the beneficiary’s side may vary, depending on the bank’s system. Within the SEPA Instant infrastructure, refunds are completed the same day, while with SEPA Credit Transfers the process may take up to 48–72 hours. Sumsub's Penny Drop Verification solution covers only those banks that process at least 80% of all payment transactions within 30 minutes.

What are the possible reasons why a payment transaction could take longer to process?

A payment transaction could take longer to process due to:

- Payer's ASPSP processing the transactions in batch, instead of real-time.

- Ongoing fraud and compliance checks conducted by the payer's ASPSP.

- The transaction being processed by the payer's ASPSP outside business hours.

What are the possible reasons why a payment transaction could be rejected?

A payment transaction may be rejected due to:

- User not completing the SCA on the ASPSP's platform.

- User denying the payment transaction authorization.

- Payment transaction being refused by the payer's ASPSP.

- User having insufficient funds in their bank account.

- User revoking the payment via their ASPSP after authorizing it.

- Transaction processing exceeding the 24-hour threshold.

What are the possible reasons why a refund transaction could be rejected?

There are no known scenarios in which the refund transaction could be left unprocessed. Sumsub will ensure that the user's payment is either automatically or manually returned to them.

Does Sumsub charge its clients per initiated or completed Penny Drop Verification session?

Sumsub's clients are charged per completed Penny Drop Verification sessions, once the end-user authorizes the transaction.

How can Sumsub's clients request an addition to the list of covered financial institutions?

Clients can submit a request to Sumsub via their dedicated Customer Success Manager to check if the desired ASPSP is available within the EU/EEA or other open banking ecosystems and supports SEPA Credit Transfers or SEPA Instant. If the bank is not already supported, Sumsub will assess processing times and the payment methods available to determine whether the ASPSP can be added.

Updated 8 days ago